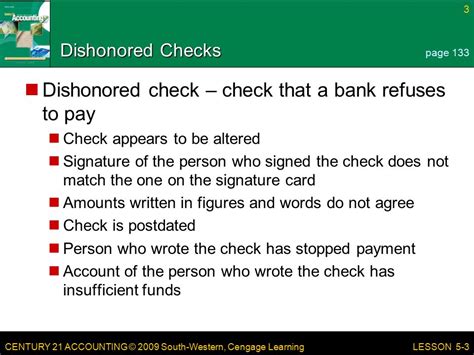

A Check That A Bank Refuses To Pay

Breaking News Today

Apr 05, 2025 · 6 min read

Table of Contents

A Check That a Bank Refuses to Pay: Understanding the Reasons and Recourse

A check, once a ubiquitous symbol of financial transactions, can sometimes become a source of frustration and financial hardship when a bank refuses to pay it. This situation, while potentially unsettling, is governed by specific legal and financial principles. Understanding why a bank might reject a check and the steps you can take to resolve the issue is crucial for both payers and payees. This comprehensive guide delves into the various reasons for check rejection, the legal ramifications, and the strategies for effective recourse.

Reasons for Bank Check Rejection

Banks employ rigorous processes to verify the legitimacy and financial soundness of checks before processing them. Several factors can trigger a bank's refusal to honor a check, broadly categorized as:

1. Insufficient Funds (NSF):

This is the most common reason for check rejection. Insufficient funds (NSF) simply means the account holder doesn't have enough money in their checking account to cover the check amount. This leads to a returned check, often with an NSF fee charged to the account holder. The payee receives a notice indicating the check was returned due to insufficient funds. The impact on the payee can range from inconvenience to serious financial consequences, particularly if the check was crucial for timely bill payment or business transaction.

2. Account Closure:

If the account on which the check was drawn has been closed, the bank will automatically reject it. This is straightforward; the account no longer exists, and there are no funds available to process the payment. The closure could be voluntary (the account holder closed it) or involuntary (the bank closed it due to inactivity, suspicious activity, or other reasons). In such cases, the payee needs to pursue alternative means of payment from the payer.

3. Stop Payment Orders:

The account holder can instruct the bank to stop payment on a specific check. This is a legitimate action, often taken to prevent fraudulent check usage or to rectify an unintentional error in payment. If a stop payment order is in place, the bank is obligated to refuse payment on the check. The payee should contact the payer to understand the reason for the stop payment and arrange for an alternative payment method.

4. Account Frozen or Legal Hold:

Banks can freeze accounts under various circumstances, such as legal action (garnishment), suspected fraud, or suspicion of money laundering. A frozen account renders any checks drawn on it invalid, leading to rejection by the bank. This situation often requires the account holder to resolve the underlying legal or financial issues before accessing their funds and issuing new checks.

5. Check Alteration or Forgery:

Banks have sophisticated systems to detect altered or forged checks. Any attempt to change the amount, payee's name, or other crucial details on a check will lead to immediate rejection. Forged checks are fraudulent and have serious legal implications for the forger. Banks have a responsibility to prevent fraudulent transactions and will reject such checks.

6. Stale-Dated Checks:

Checks that are significantly past their date of issuance are considered stale-dated. While there isn't a universally fixed timeframe for a check to become stale-dated, generally, checks older than six months are considered questionable. Banks are not obligated to honor stale-dated checks, and they often reject them to minimize the risk of fraud or errors.

7. Incorrect or Missing Information:

A check needs accurate and complete information to be processed. Missing account numbers, incorrect routing numbers, illegible signatures, or other missing information can all lead to bank rejection. The bank may attempt to contact the account holder for clarification, but if the issue remains unresolved, the check will be returned.

8. Signature Discrepancies:

Banks routinely verify signatures against the signature card on file. Any significant discrepancies between the signature on the check and the signature card will result in rejection. This is a key security measure to prevent unauthorized access to funds and fraudulent check usage.

Legal Ramifications of Check Rejection

The consequences of a bank's refusal to pay a check vary depending on the reason for rejection and the relationship between the payer and payee.

-

NSF Checks: For the payer, NSF checks result in fees and damaged credit. For the payee, it leads to financial inconvenience and potential late payment penalties. The payee may have legal recourse to recover the funds from the payer.

-

Fraudulent Checks: Forgery and alteration are serious offenses with potential criminal charges and civil lawsuits. Banks typically investigate such cases and cooperate with law enforcement.

-

Breach of Contract: If a check was issued as part of a contractual agreement and the bank refuses to pay due to the payer's fault (e.g., NSF), the payee may have grounds to sue for breach of contract.

Recourse for the Payee

If you receive a check that the bank refuses to pay, several steps can be taken:

-

Contact the Payer: The first step is to contact the payer to understand the reason for the rejection. They might be unaware of the issue (e.g., insufficient funds) and can rectify it promptly.

-

Review the Check: Carefully examine the check for any errors, such as incorrect information, alteration, or an unusual signature.

-

Resubmit the Check: If the reason for rejection is a minor error (e.g., missing information), it might be possible to correct it and resubmit the check.

-

Alternative Payment Methods: Explore alternative ways to receive payment, such as wire transfer, electronic payment, or a cashier's check.

-

Legal Action: If the payer refuses to rectify the situation or if there is evidence of fraud, you might consider legal action to recover the funds. Consult with an attorney to explore your options. Documentation, including the returned check, communication with the payer, and any related agreements, is crucial for legal action.

-

Small Claims Court: For smaller amounts, small claims court can be a relatively inexpensive and efficient way to resolve the dispute.

Preventing Check Rejection

Prevention is always better than cure. Here are some measures to minimize the risk of check rejection:

-

Maintain Sufficient Funds: Always ensure you have sufficient funds in your account to cover all outstanding checks.

-

Verify Account Information: Double-check the account number and routing number before issuing a check.

-

Use a Check Register: Maintain a careful check register to track all check issuances and balances.

-

Regular Bank Statement Review: Regularly review your bank statements to monitor your account activity and identify any potential issues.

-

Consider Alternative Payment Methods: Explore electronic payment methods, which are often safer and more efficient.

-

Protect Your Checks: Store your checks securely to prevent theft or misuse.

-

Report Lost or Stolen Checks: Immediately report lost or stolen checks to your bank to prevent fraudulent use.

Conclusion

A check rejection can be a frustrating experience, but understanding the reasons behind it and the available recourse options can help mitigate the impact. Whether you are a payer or payee, proactive measures and careful attention to detail can significantly reduce the likelihood of encountering this problem. Remember, clear communication, accurate information, and responsible financial practices are key to ensuring smooth and successful financial transactions. In situations involving substantial amounts or suspected fraud, seeking legal counsel is strongly advisable. By understanding the legal and practical aspects of check rejection, you can protect your financial interests and maintain a positive financial standing.

Latest Posts

Latest Posts

-

The Indoor Coil Is The Condenser In

Apr 06, 2025

-

Which Of The Following Is Associated With A Parameter

Apr 06, 2025

-

Men Never Greet With A Kiss In Spanish Speaking Countries

Apr 06, 2025

-

What Manipulation Technique Should Be Reported When An Fie

Apr 06, 2025

-

Which Of These Structures Stores Modifies And Packages Products

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about A Check That A Bank Refuses To Pay . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.