A Flexible Budget Performance Report Combines The

Breaking News Today

Apr 02, 2025 · 6 min read

Table of Contents

A Flexible Budget Performance Report Combines the Best of Both Worlds

Budgeting is crucial for any successful business, regardless of size or industry. It provides a roadmap for financial management, guiding resource allocation and strategic decision-making. However, traditional, static budgeting often falls short in dynamic business environments. This is where the flexible budget performance report shines. It offers a more accurate and insightful view of financial performance by adapting to actual activity levels. This article delves into the intricacies of a flexible budget performance report, explaining its benefits, components, and how to create one.

Understanding the Limitations of Static Budgets

A static budget, also known as a fixed budget, is prepared at the beginning of a period based on a predetermined level of activity. It remains unchanged throughout the period, regardless of actual sales or production volume. While providing a benchmark, its rigidity presents several drawbacks:

- Inaccuracy: If actual activity differs significantly from the budgeted activity level, the static budget provides a misleading picture of performance. Variances between the budget and actual results might be wrongly attributed to inefficiency when, in fact, they stem from changes in sales or production.

- Lack of Flexibility: Static budgets fail to adapt to unforeseen circumstances, such as changes in market demand, supply chain disruptions, or unexpected economic fluctuations. This inflexibility limits its effectiveness in managing resources dynamically.

- Demotivation: When actual results deviate significantly from a static budget, it can demotivate employees. They may feel unfairly judged when factors beyond their control influence the outcomes.

The Power of Flexible Budgeting: Adapting to Reality

A flexible budget, in contrast, is designed to adjust to changes in activity levels. It provides a more realistic and accurate assessment of performance by calculating expected costs and revenues at various activity levels. This adaptability leads to several advantages:

- Improved Accuracy: By adjusting to actual activity, a flexible budget provides a more precise comparison between budgeted and actual figures. This enhances the understanding of true performance, separating controllable and uncontrollable variances.

- Enhanced Control: The flexibility allows managers to focus on areas where performance deviates significantly from expectations, even when activity levels change. This allows for timely corrective actions and improved resource allocation.

- Increased Motivation: Employees are more likely to be motivated when performance evaluations consider factors beyond their immediate control. A flexible budget acknowledges the impact of external factors, promoting fairness and encouraging improved performance where possible.

- Better Decision-Making: A flexible budget provides a clearer picture of profitability and cost efficiency at different activity levels. This enables managers to make better informed decisions regarding pricing strategies, resource allocation, and production planning.

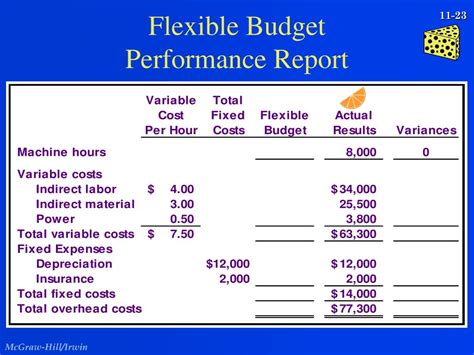

Key Components of a Flexible Budget Performance Report

A comprehensive flexible budget performance report typically includes the following components:

1. Sales Budget Variance Analysis

This section compares actual sales revenue with the flexible budget's projected revenue based on actual sales volume. The variance is analyzed to understand the factors contributing to the difference, such as pricing strategies, sales promotions, or market conditions. Key metrics include:

- Sales Price Variance: The difference between actual and budgeted selling prices, multiplied by the actual sales quantity.

- Sales Volume Variance: The difference between actual and budgeted sales quantities, multiplied by the budgeted selling price.

2. Cost of Goods Sold (COGS) Variance Analysis

This section analyzes the variance between actual COGS and the flexible budget's projected COGS based on actual production volume. This helps in identifying inefficiencies in production processes and material sourcing. Key metrics include:

- Material Price Variance: The difference between actual and budgeted material prices, multiplied by the actual quantity of materials used.

- Material Quantity Variance: The difference between actual and budgeted material quantities used, multiplied by the budgeted material price.

- Labor Rate Variance: The difference between actual and budgeted labor rates, multiplied by the actual labor hours worked.

- Labor Efficiency Variance: The difference between actual and budgeted labor hours, multiplied by the budgeted labor rate.

- Variable Overhead Variance: Analyzes variances in variable overhead costs like utilities and supplies based on actual production.

- Fixed Overhead Variance: Examines the difference between budgeted and actual fixed overhead costs.

3. Operating Expense Variance Analysis

This section compares actual operating expenses with the flexible budget's projections, categorized by variable and fixed expenses. Understanding these variances is critical to controlling operational costs. Key aspects include:

- Variable Operating Expenses: Analyze variances in expenses like sales commissions, delivery costs, and utilities based on actual sales volume.

- Fixed Operating Expenses: Compare budgeted and actual figures for expenses like rent, salaries, and insurance. Significant variances might warrant investigation.

4. Net Operating Income Variance

This is the final outcome, showcasing the overall difference between actual net operating income and the flexible budget's projection. It is the sum of all the variances analyzed previously. Understanding the drivers of this variance provides valuable insight into overall business performance.

Creating a Flexible Budget Performance Report: A Step-by-Step Guide

Preparing a flexible budget performance report involves several key steps:

-

Determine the Activity Level: Identify the key driver of costs and revenues, often units sold or produced. This will be the basis for adjusting the budget.

-

Develop a Flexible Budget: Create a budget showing expected costs and revenues at various activity levels. This typically involves identifying variable and fixed costs.

-

Gather Actual Data: Collect actual data on sales, production, costs, and expenses for the period.

-

Calculate Variances: Compare actual results with the flexible budget's projections at the actual activity level. Calculate variances for each revenue and cost component.

-

Analyze Variances: Investigate the causes of significant variances. Determine if they are due to controllable factors (e.g., inefficient production) or uncontrollable factors (e.g., changes in market demand).

-

Prepare the Report: Compile the variances into a comprehensive report, highlighting key findings and areas requiring attention. Present the information clearly and concisely, using charts and graphs where appropriate.

-

Use the Report for Improvement: Utilize the report's findings to refine budgeting processes, improve operational efficiency, and enhance future decision-making.

Beyond the Numbers: Utilizing the Report for Strategic Advantages

The flexible budget performance report is not just a financial document; it's a strategic tool. Its insights can be leveraged in several ways:

-

Performance Evaluation: It allows for a more fair and accurate assessment of employee and departmental performance, considering the impact of external factors.

-

Resource Allocation: By understanding where resources are being used most effectively (or ineffectively), companies can optimize spending and improve return on investment.

-

Pricing Strategies: Analysis of sales price variances can inform pricing decisions, helping to maximize revenue and profitability.

-

Cost Reduction Initiatives: Identifying areas with significant cost variances can lead to the implementation of targeted cost reduction programs.

-

Improved Forecasting: By learning from past variances, companies can improve the accuracy of their future budgets and forecasts.

Integrating Technology for Enhanced Flexible Budgeting

Spreadsheet software like Excel or Google Sheets can be used to create flexible budget performance reports. However, more advanced enterprise resource planning (ERP) systems provide automated tools to streamline the process. These systems can integrate data from various sources, automate variance calculations, and generate comprehensive reports.

Conclusion: Embracing Flexibility for Superior Financial Management

In conclusion, a flexible budget performance report offers a powerful alternative to static budgeting. Its adaptability to changing circumstances leads to more accurate financial insights, improved decision-making, enhanced control, and ultimately, improved business performance. By understanding its components, creating a well-structured report, and strategically utilizing its insights, businesses can achieve a significant edge in managing finances and driving growth in today's dynamic business environment. The transition from rigid, static budgeting to the dynamic, adaptable approach of flexible budgeting is a crucial step toward robust financial management and sustained success.

Latest Posts

Latest Posts

-

Increased Participation In Small Business Exporting Owes Credit To

Apr 03, 2025

-

Which Of The Following Is An Example Of Explicit Knowledge

Apr 03, 2025

-

By The 20th Week Of Pregnancy Emt

Apr 03, 2025

-

What Is The Goal Of The Insider Threat Program

Apr 03, 2025

-

An Adult Patient Who Is Not Experiencing Difficulty Breathing Will

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about A Flexible Budget Performance Report Combines The . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.