An Annuity Pays Benefits Based On Units

Breaking News Today

Apr 03, 2025 · 6 min read

Table of Contents

Annuities That Pay Benefits Based on Units: A Comprehensive Guide

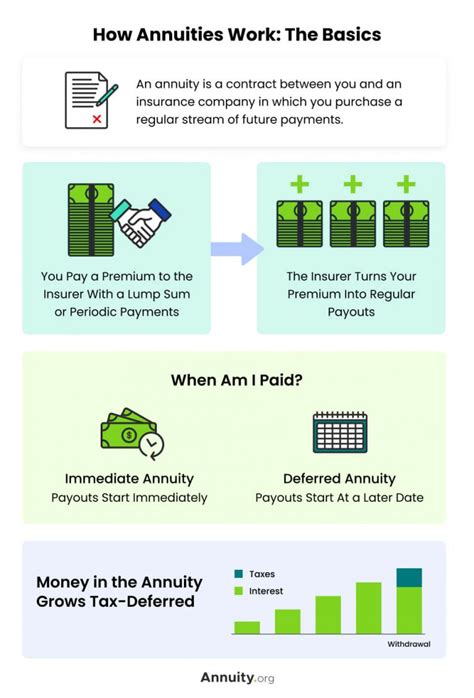

Annuities are financial instruments designed to provide a steady stream of income, often during retirement. While many annuities pay benefits based on a fixed dollar amount or a variable amount tied to market performance, a less common but equally important type uses a unit-based payout system. Understanding how these annuities work is crucial for anyone considering them as part of their retirement plan. This comprehensive guide delves into the intricacies of unit-based annuity payouts, exploring their advantages, disadvantages, and suitability for different investor profiles.

Understanding Unit-Based Annuity Payouts

A unit-based annuity, unlike its fixed or variable counterparts, distributes payments based on the number of units the annuitant owns and the current unit value. This value fluctuates, usually mirroring the performance of an underlying investment portfolio. Think of it like owning shares in a mutual fund, but instead of receiving dividends, you receive regular payments based on the value of your "shares" (units).

Key Features of Unit-Based Annuities:

- Unit Value Fluctuation: The core characteristic. The value of each unit rises and falls with the performance of the underlying investments. This means your payout can increase or decrease over time.

- Regular Payments: Payments are typically made monthly, quarterly, or annually, but the specific frequency is determined during the annuity purchase.

- Investment Portfolio: The underlying investments can range from conservative bonds to more aggressive stocks and alternative assets. The investment strategy chosen significantly impacts the potential growth and stability of the unit value.

- Guaranteed Minimum: Some unit-based annuities offer a guaranteed minimum income, protecting against extreme market downturns. This guarantee often comes with a higher initial cost.

- Annuitization Phase: After the accumulation phase (where you contribute to the annuity), the annuitization phase begins. This is when you start receiving regular payments based on your accumulated units and their current value.

How Unit-Based Annuity Payments are Calculated

Calculating the payout involves a relatively straightforward formula:

Total Payment = Number of Units Owned * Current Unit Value * Payment Frequency Factor

The Payment Frequency Factor adjusts the payment to reflect whether you receive payments monthly, quarterly, or annually.

For example:

Let's say you own 100 units, the current unit value is $10, and you receive monthly payments. Assuming a payment frequency factor of 1/12 (for monthly payments), your monthly payment would be:

100 units * $10/unit * (1/12) = $83.33

However, remember that the current unit value ($10 in this example) is dynamic and changes based on market performance. If the unit value increases to $12, your monthly payment would also rise to $100. Conversely, a decrease in unit value would lead to a lower monthly payment.

Advantages of Unit-Based Annuities

Unit-based annuities offer several benefits:

- Potential for Higher Returns: The linkage to market performance allows for the potential to earn higher returns compared to fixed annuities, especially in bull markets. This is because the investment portfolio is actively managed, aiming to grow the unit value over time.

- Flexibility in Investment Strategy: You often have choices in the underlying investment portfolio, allowing you to tailor the risk level to your comfort and financial goals. You might opt for a conservative, balanced, or aggressive investment approach.

- Inflation Hedge (Potentially): If the unit value keeps pace with or surpasses inflation, your purchasing power remains relatively stable. However, this is not guaranteed.

- Simplicity in Understanding Payouts: The formula for calculating payouts is clear. It is easier to comprehend than the more complex calculation methods of some variable annuities.

- Tax Advantages: Similar to other annuities, unit-based annuities often offer tax-deferred growth, meaning you only pay taxes on the income portion of your payments during retirement.

Disadvantages of Unit-Based Annuities

While offering attractive features, unit-based annuities also have drawbacks:

- Market Risk: The biggest disadvantage is the inherent risk associated with market fluctuations. A downturn in the market can significantly reduce the unit value and your monthly payments, potentially impacting your retirement income.

- Complexity: While the payout calculation is simple, the underlying investment strategies can be quite complex. Understanding the intricacies of the investment portfolio and its potential risks requires careful consideration.

- Fees: Unit-based annuities usually come with fees like management fees, expense ratios, and mortality and expense risk charges, which can reduce your overall returns.

- Lack of Guaranteed Lifetime Income: Unless you choose an annuity with a guaranteed minimum income, there’s no assurance of receiving payments for your entire lifetime. Your income stream depends entirely on the performance of the underlying investments.

- Surrender Charges: Similar to other annuities, withdrawing funds before a specified period can incur surrender charges, impacting your overall returns.

Unit-Based Annuities vs. Other Annuity Types

Understanding how unit-based annuities compare to other types is crucial for making informed decisions.

Unit-Based vs. Fixed Annuities:

| Feature | Unit-Based Annuity | Fixed Annuity |

|---|---|---|

| Payout | Based on unit value and number of units | Fixed dollar amount |

| Risk | High (market risk) | Low (no market risk) |

| Return Potential | High | Low |

| Guaranteed Income | Usually not, unless specified | Guaranteed for a specified period |

Unit-Based vs. Variable Annuities:

While both are subject to market fluctuations, key differences exist:

| Feature | Unit-Based Annuity | Variable Annuity |

|---|---|---|

| Payout Calculation | Simpler, directly tied to unit value | More complex, based on sub-accounts |

| Investment Choices | Often fewer choices | Often a wider range of sub-accounts |

| Fees | Generally lower fee structure | Can have higher fees |

Who Should Consider a Unit-Based Annuity?

Unit-based annuities are not a one-size-fits-all solution. They are best suited for:

- Investors with a higher risk tolerance: Due to market risk, those comfortable with potential fluctuations in income are better suited.

- Investors seeking potential for higher returns: If your goal is to potentially maximize retirement income, the higher return potential of unit-based annuities might align with your strategy.

- Investors who understand investment risks: You need to be comfortable understanding investment strategies and market fluctuations.

- Long-term investors: Because of the potential for short-term losses and fees, a long-term investment horizon is more suitable.

Things to Consider Before Investing

Before investing in a unit-based annuity, it’s crucial to:

- Assess your risk tolerance: Honestly evaluate your comfort level with market fluctuations.

- Understand the fees: Carefully review all associated fees and charges to determine their impact on your returns.

- Compare different annuity options: Shop around and compare options from different providers to find the best fit for your needs and risk tolerance.

- Seek professional financial advice: Consulting a qualified financial advisor can provide personalized recommendations based on your specific financial circumstances and goals.

Conclusion: Navigating the World of Unit-Based Annuities

Unit-based annuities offer a unique approach to retirement income planning. Their ability to potentially provide higher returns and adjust to market conditions is appealing to some investors. However, the inherent market risk and complexity require careful consideration. By thoroughly understanding the advantages and disadvantages, comparing different options, and seeking professional advice, you can make an informed decision about whether a unit-based annuity is the right choice for your retirement strategy. Remember that responsible investing and diversification remain essential components of a robust financial plan.

Latest Posts

Latest Posts

-

Answer Key For Saxon Math Course 3

Apr 04, 2025

-

A Return Of Merchandise To The Vendor Results In A

Apr 04, 2025

-

As A Single Adult You Should

Apr 04, 2025

-

How Many Zones Are There In The Zone Control System

Apr 04, 2025

-

Explain How Oil Paint Is Made What Is The Vehicle

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about An Annuity Pays Benefits Based On Units . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.