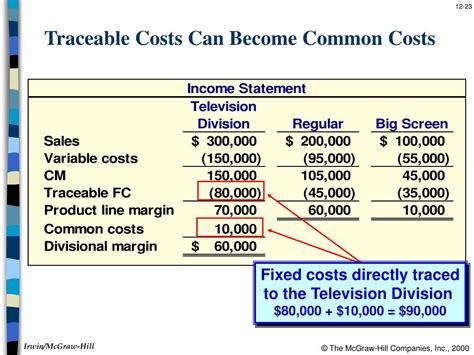

Costs That Can Be Traced Directly To A Segment

Breaking News Today

Mar 28, 2025 · 6 min read

Table of Contents

Costs Directly Traceable to a Segment: A Comprehensive Guide

Understanding how to accurately allocate costs to specific segments of your business is crucial for effective decision-making and profitability. This detailed guide explores the intricacies of directly traceable costs, providing a comprehensive overview of their identification, allocation, and importance in strategic planning. We'll delve into various examples, methodologies, and potential challenges, equipping you with the knowledge to confidently manage your business segments.

What are Directly Traceable Costs?

Directly traceable costs, also known as directly attributable costs, are expenses that can be specifically and definitively linked to a particular segment or product line within your business. Unlike indirect costs (overhead), which are shared across multiple segments and require allocation based on certain criteria, directly traceable costs are easily identifiable and assigned. This straightforward attribution allows for more accurate segment profitability analysis and informed decision-making.

Key Characteristics of Directly Traceable Costs:

- Direct Association: The cost is specifically incurred as a direct result of the operations of a particular segment.

- Measurable and Identifiable: The cost can be precisely measured and directly linked to the segment's activity.

- Easy Allocation: No complex allocation methods are required; the cost is inherently tied to the segment.

Examples of Directly Traceable Costs:

The specific types of directly traceable costs will vary depending on your industry and business model. However, some common examples include:

Manufacturing Businesses:

- Direct Materials: Raw materials directly used in the production of goods for a specific segment. For example, the cost of cotton used in producing a specific line of t-shirts.

- Direct Labor: Wages and salaries paid to employees directly involved in the production or delivery of goods or services for a specific segment. This includes wages paid to assembly line workers dedicated to a particular product line.

- Specific Equipment Costs: The depreciation or lease payments for machinery used exclusively in the production of goods for a particular segment. For example, the cost of a specialized printing press only used for a certain type of packaging.

Service Businesses:

- Sales Commissions: Commissions paid to salespeople directly associated with sales generated within a specific segment.

- Direct Marketing Expenses: Costs associated with marketing campaigns explicitly targeting a particular segment, such as targeted advertising campaigns or specific promotional materials.

- Customer Service Costs: Costs directly related to serving customers within a specific segment, such as dedicated customer support lines or specialized training for support staff.

Retail Businesses:

- Product-Specific Costs: Costs directly related to purchasing and stocking a specific product line within a segment.

- Shelf Space Rent: Rent for shelf space allocated exclusively to a particular product line within a specific segment. For a supermarket, this would mean the space allocated for a specific brand of cereal.

- Segment-Specific Staff: Salaries for staff members dedicated to managing a specific segment, like a dedicated manager for the electronics department in a department store.

Methods for Identifying Directly Traceable Costs:

Proper identification is paramount for accurate cost allocation. Several methods can be employed:

- Detailed Cost Accounting: Implementing a robust cost accounting system that meticulously tracks all expenses, allowing for easy identification of costs associated with each segment.

- Activity-Based Costing (ABC): ABC focuses on identifying and assigning costs based on the activities that drive costs. This method can help identify more precise directly traceable costs, particularly in complex business environments.

- Regular Cost Reviews: Conducting periodic reviews of expenses to ensure costs are correctly categorized and allocated. This helps catch any discrepancies or changes that might affect the classification of costs.

- Detailed Invoices and Purchase Orders: Maintaining detailed records of invoices and purchase orders helps in tracing costs to their respective segments.

Importance of Accurate Cost Allocation:

The accurate allocation of directly traceable costs is vital for several key reasons:

- Segment Profitability Analysis: It allows for a clear picture of the profitability of each segment, enabling better decision-making regarding resource allocation and investment strategies.

- Pricing Decisions: Understanding the direct costs associated with a segment allows for setting appropriate prices to ensure profitability.

- Performance Evaluation: Accurate cost allocation is crucial for evaluating the performance of different segments and identifying areas for improvement or potential cost reduction.

- Strategic Planning: It provides valuable insights for strategic planning and decision-making regarding product lines, market segments, and overall business strategy. Knowing which segments are profitable and which are not allows for targeted investment and divestment strategies.

- Resource Allocation: Understanding costs helps to efficiently allocate resources to the most profitable segments and streamline operations.

Challenges in Identifying Directly Traceable Costs:

While straightforward in concept, accurately identifying directly traceable costs can present some challenges:

- Joint Costs: Some costs may benefit multiple segments, making it difficult to directly attribute them to a single segment. These require allocation methods such as allocation based on revenue or units produced.

- Shared Resources: Shared resources, such as administrative staff or shared facilities, present a challenge in allocating costs directly to individual segments. This necessitates cost allocation methods such as the allocation of overhead based on a chosen cost driver.

- Complex Business Models: In businesses with intricate product lines or diverse service offerings, it can be challenging to accurately trace costs to individual segments. A clear organizational structure and cost accounting systems are crucial in such cases.

- Data Accuracy: Inaccurate or incomplete data can lead to misallocation of costs, impacting the accuracy of segment profitability analysis. Regular data validation and reconciliation are key to maintain accuracy.

Addressing Challenges: Cost Allocation Methods

When faced with challenges in directly tracing costs, various allocation methods can be employed to distribute indirect costs more fairly. These methods include:

- Revenue-Based Allocation: Allocate costs proportionally to the revenue generated by each segment. This is a straightforward method but may not accurately reflect the true cost drivers.

- Activity-Based Allocation: Allocates costs based on the consumption of resources by each segment. This offers a more refined approach, considering various activities driving costs.

- Units-Produced Allocation: Ideal for manufacturing businesses, allocating costs based on the number of units produced by each segment.

- Space-Based Allocation: Applicable for retail and office settings, allocating costs based on the space occupied by each segment.

- Direct Labor Hours Allocation: A common method for manufacturing where costs are distributed based on the direct labor hours spent on each segment.

The choice of allocation method depends on the specific circumstances and the nature of the business. It's crucial to select a method that is both fair and accurately reflects the cost drivers for each segment.

Integrating Technology for Enhanced Cost Tracking:

Modern business management systems significantly aid in identifying and tracking directly traceable costs:

- Enterprise Resource Planning (ERP) Systems: ERP systems integrate various business functions, providing a centralized platform for tracking expenses and allocating costs across different segments.

- Cost Accounting Software: Specialized cost accounting software helps to automate cost tracking and reporting, providing a clear view of cost allocation.

- Data Analytics Tools: Data analytics tools can help analyze cost data, identifying patterns and trends that can inform better cost allocation strategies.

Conclusion:

Accurately identifying and allocating directly traceable costs is a cornerstone of sound financial management and strategic decision-making. By implementing robust cost accounting systems, employing appropriate cost allocation methods, and leveraging technological advancements, businesses can gain invaluable insights into segment profitability, optimize resource allocation, and improve overall performance. The commitment to accuracy in this area will contribute to a more informed and successful business future. Regular review and refinement of your cost allocation strategies will ensure your business remains agile and responsive to changes in your market.

Latest Posts

Latest Posts

-

Common Signs And Symptoms Of A Hypertensive Emergency Include Quizlet

Mar 31, 2025

-

2020 Practice Exam 3 Mcq Ap Lang Quizlet

Mar 31, 2025

-

Check The Vds To See If Quizlet

Mar 31, 2025

-

An Implied Power Is One That Quizlet

Mar 31, 2025

-

Chapter 12 Lord Of The Flies Quizlet

Mar 31, 2025

Related Post

Thank you for visiting our website which covers about Costs That Can Be Traced Directly To A Segment . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.