Jonas Is A Whole Life Insurance Policyowner

Breaking News Today

Apr 02, 2025 · 6 min read

Table of Contents

Jonas Is a Whole Life Insurance Policyowner: Understanding the Implications

Jonas, like many individuals, has chosen a whole life insurance policy. This decision carries significant implications for his financial future, offering both benefits and considerations. Let's delve deep into the world of whole life insurance through Jonas's experience, exploring its intricacies and providing a comprehensive understanding of this financial instrument.

What is Whole Life Insurance?

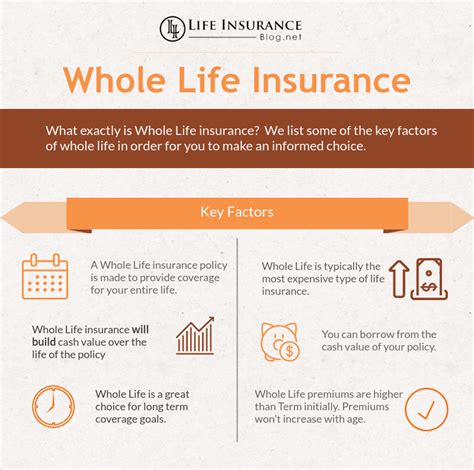

Whole life insurance, unlike term life insurance which provides coverage for a specified period, offers lifelong coverage as long as premiums are paid. It combines a death benefit with a cash value component that grows tax-deferred over time. This cash value element is a key differentiator and a significant aspect of Jonas's financial planning.

Key Features of Jonas's Whole Life Policy

Jonas's whole life policy likely includes several key features:

-

Guaranteed Lifetime Coverage: The most significant feature is the lifelong protection it offers. This provides peace of mind knowing his beneficiaries will receive a death benefit regardless of when he passes away, barring any lapses in premium payments.

-

Cash Value Accumulation: A crucial aspect of whole life insurance is the cash value component. This grows over time, earning interest at a rate specified by the insurance company. This growth is tax-deferred, meaning Jonas won't pay taxes on the earnings until he withdraws them.

-

Policy Loans: Jonas can borrow against the cash value of his policy without affecting the death benefit. This can provide a valuable source of funds for emergencies or other financial needs. However, it's crucial to understand the implications of borrowing against the policy, including interest charges and potential reduction in the death benefit if the loan isn't repaid.

-

Dividends (in Participating Policies): Some whole life policies, like Jonas's might be participating, meaning he may receive dividends from the insurance company's profits. These dividends are not guaranteed, but they can provide additional value and potentially increase the cash value of his policy over time. He can choose how to use these dividends – reinvesting them in the policy to accelerate cash value growth, taking them as cash, or using them to reduce future premiums.

-

Premium Payment Options: Jonas likely has flexibility in how he pays his premiums. Options might include level premiums (fixed amount each year), flexible premiums (allowing adjustments based on his financial situation), or single premium payments (a lump sum paid upfront).

The Financial Implications for Jonas

Jonas's decision to own a whole life insurance policy has profound financial implications, influencing his:

1. Estate Planning:

-

Death Benefit for Beneficiaries: The policy's death benefit provides financial security for Jonas's designated beneficiaries after his passing. This can help cover funeral expenses, debts, and ongoing living expenses for his dependents. He can name specific beneficiaries or create a trust to manage the distribution of the death benefit.

-

Asset Protection: The death benefit is generally exempt from estate taxes, shielding a significant portion of his assets from taxation. This is a crucial aspect of estate planning, especially for high-net-worth individuals.

-

Legacy Planning: Beyond immediate financial support, the death benefit can help Jonas leave a lasting legacy for his family. This can provide financial stability for future generations, enabling them to pursue education or other opportunities.

2. Retirement Planning:

-

Supplemental Retirement Income: Jonas can access the cash value of his policy during retirement. He can withdraw funds systematically or use the policy as collateral for loans, providing a supplementary income stream alongside other retirement savings.

-

Tax Advantages: The tax-deferred growth of the cash value provides a significant tax advantage compared to some other investment vehicles. This means more of his money remains invested, potentially leading to greater accumulation over time.

-

Guaranteed Minimum Return: While the rate of return on the cash value may not be as high as other investments, it offers a guaranteed minimum, providing a level of certainty not found in more volatile investment options. This predictability can be very appealing to risk-averse individuals like Jonas.

3. Long-Term Financial Security:

-

Protection Against Unexpected Expenses: The policy offers a financial safety net, protecting Jonas's family from the devastating impact of unforeseen events, such as severe illness or job loss. The cash value component can provide access to funds without impacting the death benefit.

-

Inflation Hedge: Over the long term, the cash value of the policy may help offset the effects of inflation, preserving the purchasing power of the death benefit and accumulated savings. The consistent growth, even if modest, provides a stable foundation against economic fluctuations.

-

Financial Stability: Owning a whole life policy can provide a sense of financial stability, knowing that he has a plan in place to protect his family's future regardless of unforeseen circumstances. This peace of mind is often a key factor in choosing this type of insurance.

Considerations for Jonas

While whole life insurance offers many advantages, Jonas needs to consider several factors:

1. Premium Costs:

Whole life insurance premiums are typically higher than term life insurance premiums because of the lifelong coverage and cash value component. Jonas needs to carefully assess whether the higher premiums align with his budget and financial goals. He should carefully compare the cost of whole life against other savings and investment options.

2. Fees and Charges:

Jonas needs to understand all fees and charges associated with his policy, including administrative fees, mortality charges, and any surrender charges if he decides to cancel the policy before maturity. These fees can impact the overall return on his investment. Transparency regarding these fees is paramount.

3. Cash Value Growth Rate:

The cash value growth rate isn't guaranteed and may be lower than the returns offered by some other investments. Jonas needs to manage expectations regarding the rate of growth and understand that it will likely fluctuate over time. He should compare the expected growth to other investment opportunities.

4. Policy Surrender:

If Jonas decides to surrender his policy, he may face surrender charges, potentially reducing the amount he receives. Understanding these charges is crucial before making a decision to surrender the policy, especially in the early years. Understanding the financial implications of this decision should be paramount.

5. Alternative Investment Options:

Jonas should carefully compare whole life insurance to other investment options, such as mutual funds, stocks, or bonds, to determine if it aligns with his overall financial goals and risk tolerance. A thorough financial assessment should be conducted to make an informed decision.

Conclusion: Navigating Jonas's Whole Life Insurance Journey

Jonas's journey as a whole life insurance policyowner highlights the complexities and long-term implications of this financial instrument. While it offers significant benefits in estate planning, retirement planning, and long-term financial security, it's crucial to understand the costs, fees, and potential limitations. Careful consideration of these factors, coupled with a thorough understanding of his financial goals and risk tolerance, will ensure that Jonas makes an informed decision that aligns with his overall financial wellbeing. Regular review and professional advice can help him optimize the benefits of his policy throughout his life. This detailed examination underscores the importance of seeking professional financial advice when considering whole life insurance and regular reviews to ensure the policy remains aligned with changing life circumstances and financial goals. This holistic approach will maximize the potential benefits and minimize any potential drawbacks, ensuring Jonas's financial security and legacy.

Latest Posts

Latest Posts

-

Potential Buyers Within A Market Segment Should Be

Apr 03, 2025

-

American Heart Association Basic Life Support Exam A Answers

Apr 03, 2025

-

Which Is An Appropriate Expected Outcome For A Client

Apr 03, 2025

-

A Complete And Accurate Medical Record Provides Legal Protection For

Apr 03, 2025

-

How Is Carbon Reintroduced Into The Atmosphere

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about Jonas Is A Whole Life Insurance Policyowner . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.