The Law Of Increasing Opportunity Costs States That

Breaking News Today

Mar 22, 2025 · 5 min read

Table of Contents

The Law of Increasing Opportunity Costs: Why More Isn't Always Better

The world of economics is full of fascinating principles that govern how we produce, consume, and distribute resources. One such principle, fundamental to understanding production possibilities and resource allocation, is the Law of Increasing Opportunity Costs. This seemingly simple concept has profound implications for businesses, governments, and individuals alike. Understanding this law is crucial for making informed decisions about resource utilization and maximizing efficiency. This article delves deep into the intricacies of the Law of Increasing Opportunity Costs, exploring its underlying mechanisms, practical applications, and exceptions.

Understanding Opportunity Cost

Before diving into the law itself, let's clarify the core concept of opportunity cost. Opportunity cost represents the value of the next best alternative forgone when making a decision. It's not just about the monetary cost; it encompasses all the potential benefits you miss out on by choosing one option over another. For instance, if you spend your Saturday afternoon watching a movie, the opportunity cost isn't just the price of the ticket; it's also the potential enjoyment you could have experienced by spending that time reading a book, exercising, or spending time with loved ones.

This concept is crucial because it highlights the scarcity of resources. We simply cannot have everything we want; we must make choices. Understanding opportunity costs helps us evaluate those choices more effectively and determine which option offers the greatest overall benefit.

The Law of Increasing Opportunity Costs: A Deeper Dive

The Law of Increasing Opportunity Costs states that as we produce more of a good or service, the opportunity cost of producing each additional unit increases. This isn't a linear relationship; it's an accelerating curve. This means that the sacrifice required to produce more of one good becomes progressively greater as production increases. This is primarily due to the specialization of resources and their varying suitability for different production processes.

Why Does Opportunity Cost Increase?

Several factors contribute to the increasing opportunity cost:

-

Resource Specialization: Resources are not perfectly adaptable. Some resources are better suited for producing certain goods than others. As we produce more of a particular good, we may need to utilize resources that are less efficient in producing that good, leading to a higher opportunity cost. Imagine a farmer switching from growing wheat to growing corn. Initially, some land may be easily converted, but as more corn is planted, less suitable land (perhaps hilly or less fertile) will need to be used, resulting in a lower wheat yield per unit of land sacrificed.

-

Diminishing Returns: The principle of diminishing returns states that as we add more of one input (e.g., labor) while holding others constant (e.g., land), the increase in output will eventually diminish. This means that adding more resources may yield smaller and smaller increases in output, further increasing the opportunity cost.

-

Resource Heterogeneity: Resources are diverse and differ in their quality and productivity. As we shift resources from one production activity to another, we start using less efficient resources, which leads to a higher opportunity cost.

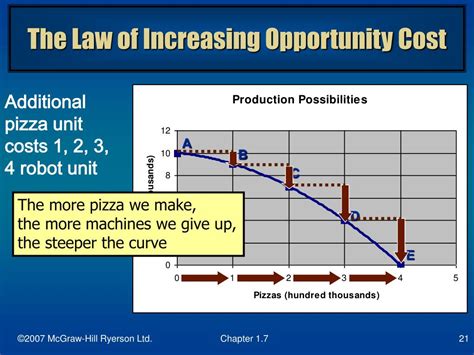

Graphical Representation

The Law of Increasing Opportunity Costs is often illustrated using a Production Possibilities Frontier (PPF) graph. The PPF is a curve that shows the maximum possible combinations of two goods that can be produced with given resources and technology. A bowed-outward PPF visually represents the law; the slope of the curve becomes steeper as we move along it, demonstrating the increasing opportunity cost.

Imagine a simplified economy producing only two goods: computers and cars. The PPF would show various combinations of computer and car production. As we shift resources from car production to computer production, the opportunity cost of producing each additional computer increases because we are using resources increasingly less suited for computer production.

Real-World Applications of the Law

The implications of the Law of Increasing Opportunity Costs are far-reaching and affect numerous aspects of our lives:

-

Government Policy: Governments constantly face choices about resource allocation. Decisions about defense spending versus healthcare, infrastructure development versus education, all involve opportunity costs. Understanding the law helps policymakers make informed decisions about maximizing societal welfare.

-

Business Decisions: Businesses must make similar choices, deciding how to allocate resources among different products or services. A company might choose to focus on a single product line to maximize efficiency, recognizing the increasing opportunity cost of diversifying into unrelated areas.

-

Individual Choices: Individuals constantly face trade-offs. The decision to work overtime means sacrificing leisure time; studying for an exam means giving up time for other activities. Recognizing these opportunity costs allows for better decision-making.

Exceptions and Limitations

While the Law of Increasing Opportunity Costs holds true in most scenarios, there can be exceptions:

-

Technological Advancements: Technological breakthroughs can alter the production possibilities and reduce opportunity costs. New technologies can increase the efficiency of resource utilization, making it possible to produce more of both goods without incurring significantly higher opportunity costs.

-

External Factors: External factors such as natural disasters or economic crises can dramatically affect resource availability and shift the PPF, temporarily altering the relationship between opportunity costs.

-

Economies of Scale: In some cases, large-scale production can lead to economies of scale, where the average cost of production decreases as output increases. This can temporarily counteract the effect of increasing opportunity costs.

Conclusion: Embracing the Inevitability of Choice

The Law of Increasing Opportunity Costs is a fundamental principle that underlies many economic decisions. It underscores the importance of careful planning and resource allocation. Recognizing that resources are scarce and that every choice carries an opportunity cost is essential for individuals, businesses, and governments alike. By understanding this law, we can make more informed decisions, maximize the utilization of available resources, and ultimately, improve our overall well-being. The challenge lies not in avoiding opportunity costs (which is impossible), but in consciously choosing the options that best align with our goals, recognizing the inherent trade-offs involved. This conscious awareness makes the seemingly abstract principle of increasing opportunity costs a powerful tool in navigating the complexities of economic decision-making. The law serves as a constant reminder: there's no such thing as a free lunch. Every choice has a cost, and those costs tend to increase the more we pursue a single path. Efficient resource allocation is about minimizing those costs, not eliminating them entirely.

Latest Posts

Latest Posts

-

What Can Readers Conclude About Allison Check All That Apply

Mar 22, 2025

-

One Of The Best Ways To Test Yourself Is To

Mar 22, 2025

-

The Etiology For Mental Disorders Is A Description Of Its

Mar 22, 2025

-

La Semana Santa Se Celebra Despues De Pascua

Mar 22, 2025

-

Paper Based Pii Is Involved In Data Breaches

Mar 22, 2025

Related Post

Thank you for visiting our website which covers about The Law Of Increasing Opportunity Costs States That . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.