Understanding A Credit Card Statement Answer Key

Breaking News Today

Apr 02, 2025 · 6 min read

Table of Contents

Understanding Your Credit Card Statement: A Comprehensive Guide

Decoding your credit card statement might seem daunting at first, but understanding its components is crucial for managing your finances effectively. This comprehensive guide will walk you through every section, providing a clear answer key to help you navigate the intricacies of your monthly statement and empower you to make informed financial decisions.

Key Sections of Your Credit Card Statement

Your credit card statement, while varying slightly between issuers, typically includes these key sections:

1. Account Information

This section displays your essential account details:

- Account Number: Your unique identifier for this specific credit card account. Keep this number secure.

- Cardholder Name: The name printed on your credit card.

- Billing Cycle: The period covered by the statement (e.g., June 1st to June 30th). Understanding the billing cycle is fundamental to tracking your spending and due dates.

- Statement Date: The date the statement was generated and sent to you.

- Previous Balance: The amount you owed at the beginning of the billing cycle. This is your starting point for understanding your current balance.

2. Transactions (Purchases & Payments)

This is the heart of your statement, detailing all your transactions during the billing cycle:

- Transaction Date: The date each purchase or payment was processed.

- Description: A brief description of the transaction (e.g., "AMAZON.COM," "Grocery Store," "Payment"). This helps you quickly categorize your spending.

- Amount: The cost of each transaction. Pay close attention to these amounts to spot any errors or unauthorized charges.

- Type of Transaction: Clear labeling distinguishes purchases, payments, credits, fees, and interest charges. This clarity aids in budgeting and expense tracking.

Understanding Transaction Details:

- Purchases: These are all the goods and services you bought using your credit card. Review these carefully for accuracy.

- Payments: These are the payments you made towards your credit card balance during the billing cycle.

- Credits: These are amounts added back to your account, such as returns, refunds, or adjustments.

- Fees: These are charges added to your account, such as late payment fees, over-limit fees, or foreign transaction fees. Understanding these fees is vital for responsible credit card use.

- Interest Charges: This is the interest accrued on your outstanding balance during the billing cycle. High interest rates can quickly inflate your debt, so understanding how interest is calculated is critical.

3. Payments and Credits Section

This section provides a clear breakdown of payments and credits applied to your account.

- Payments Made: Shows the dates and amounts of any payments you've made during the billing cycle. This section allows for easy reconciliation of payments with your records.

- Credits Applied: Lists any credits received, such as refunds or adjustments. Understanding these credits ensures you're accurately tracking your spending and balance.

4. Charges and Fees Section

This section itemizes all additional charges during the billing cycle.

- Late Payment Fees: A penalty charged if you didn't make your minimum payment by the due date. Avoid these fees by paying on time.

- Over-limit Fees: Charged if your spending exceeds your credit limit.

- Foreign Transaction Fees: Fees for using your card in a foreign currency.

- Annual Fee: (If applicable) the annual membership fee charged for your credit card.

- Other Fees: Any other fees applied during the billing cycle, such as balance transfer fees or cash advance fees.

Understanding the Impact of Fees:

These fees significantly impact your overall credit card costs. By understanding what triggers them, you can proactively avoid incurring unnecessary charges.

5. Current Balance Section

This section summarizes your financial standing at the end of the billing cycle.

- New Balance: The total amount you owe after considering all transactions, payments, and credits. This is your starting point for the next billing cycle.

- Minimum Payment Due: The minimum amount you need to pay to avoid late payment fees. While paying only the minimum keeps your account current, it increases interest charges over time, extending the repayment period significantly.

- Payment Due Date: The deadline for making your payment to avoid late fees. Mark this date prominently in your calendar.

The Importance of Minimum Payment vs. Full Payment:

While the minimum payment avoids late fees, it significantly increases the overall cost of your credit card debt. Aim to pay your balance in full each month whenever possible to avoid interest charges entirely.

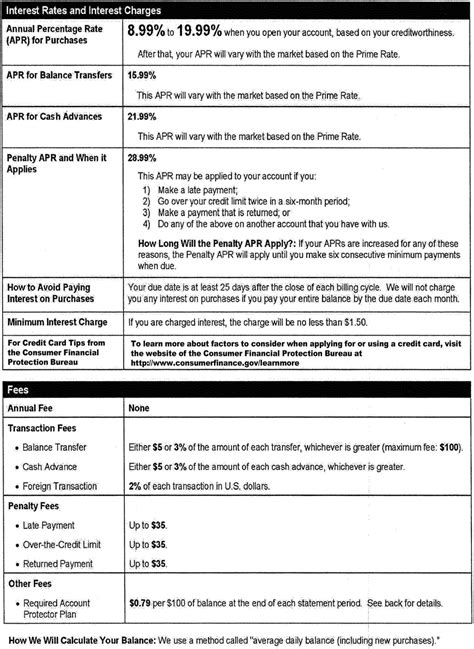

6. Interest Calculation

This section details how your interest charges are calculated. It often uses methods like the average daily balance method or the previous balance method. Understanding this calculation is crucial to controlling your interest costs.

- Average Daily Balance: Calculated by adding your daily balance throughout the billing cycle, dividing by the number of days. Interest is then charged on this average.

- Previous Balance Method: Interest is calculated based on the balance at the beginning of the billing cycle.

Interest Rate and APR:

The Annual Percentage Rate (APR) is the annual interest rate charged on your outstanding balance. A higher APR means higher interest charges. Shop around for low-APR cards if you intend to carry a balance.

7. Credit Limit and Available Credit

This section shows your credit limit and how much credit you have available. Avoid exceeding your credit limit to avoid fees and a negative impact on your credit score.

- Credit Limit: The maximum amount you can charge to your credit card.

- Available Credit: The difference between your credit limit and your current balance.

8. Contact Information and Customer Service

This section provides the contact information for your credit card issuer if you have any questions or disputes.

Spotting Errors and Disputes

Always scrutinize your statement carefully for any discrepancies.

- Unauthorized Transactions: Immediately report any transaction you didn't authorize.

- Incorrect Charges: Contact your credit card issuer to dispute any incorrect charges.

- Mathematical Errors: Verify all calculations to ensure accuracy.

Improving Your Credit Card Management

Understanding your credit card statement is fundamental to responsible credit card management. Here are some practical tips:

- Track your spending regularly: Using budgeting apps or spreadsheets can help you monitor your spending habits.

- Pay your balance in full each month: Avoid interest charges by paying your balance before the due date.

- Set up automatic payments: Avoid late fees by automating your payments.

- Check your credit report regularly: Review your credit report for accuracy and identify any potential problems.

- Maintain a low credit utilization ratio: Keeping your credit utilization ratio (the amount you owe divided by your credit limit) low can positively impact your credit score.

- Choose the right credit card: Select a credit card with features that align with your financial goals and spending habits. Consider rewards programs, low APRs, and other benefits.

- Read the fine print: Carefully review your credit card agreement to understand the terms and conditions.

Conclusion

Mastering your credit card statement empowers you to take control of your finances. By understanding each section and proactively managing your spending and payments, you can avoid unnecessary fees, improve your credit score, and make informed financial decisions. Regularly reviewing your statement is a proactive step towards financial wellness. Remember, responsible credit card use is a key element of building strong credit and achieving your financial goals. Don't hesitate to reach out to your credit card issuer's customer service if you have any questions or need further clarification.

Latest Posts

Latest Posts

-

Which Part Of A Sink Prevents Backflow Of Dirty Water

Apr 03, 2025

-

To Reduce The Risk Of Decompression Sickness Dcs I Should

Apr 03, 2025

-

The Normal Current Rating Of A Circuit Breaker Is Located

Apr 03, 2025

-

Which Task Requires Da Pam 700 107 Guidance

Apr 03, 2025

-

Why Was The Berlin Wall Called A Canvas Of Concrete

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about Understanding A Credit Card Statement Answer Key . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.