Which Financing Option Has The Highest Overall Costs

Breaking News Today

Mar 21, 2025 · 6 min read

Table of Contents

Which Financing Option Has the Highest Overall Costs? A Deep Dive into Borrowing

Choosing the right financing option can be a daunting task, especially when you're faced with a myriad of choices each promising attractive terms. However, understanding the true cost of borrowing is crucial for making informed financial decisions. While interest rates are a significant factor, the overall cost encompasses a wider range of fees and charges that can significantly impact your bottom line. This comprehensive guide will delve into various financing options, comparing their associated costs to determine which generally carries the highest overall expense. We'll explore everything from mortgages and auto loans to payday loans and credit cards, examining the nuances of each to paint a complete picture.

Understanding the Components of Financing Costs

Before we compare specific financing options, it's essential to understand the different components that contribute to the overall cost:

1. Interest Rates: The Core Cost

Interest rates represent the cost of borrowing money. A higher interest rate means you'll pay more in interest over the loan's lifetime. This is a primary driver of overall cost and often the most prominently advertised feature. However, it's only part of the story.

2. Fees and Charges: The Hidden Costs

Many financing options come with associated fees that can significantly add to the total cost. These can include:

- Origination Fees: Charged upfront by lenders to process your loan application.

- Application Fees: A fee for submitting a loan application, regardless of approval.

- Prepayment Penalties: Penalties imposed for paying off a loan early.

- Late Payment Fees: Penalties for missed or late payments.

- Annual Fees: Recurring fees charged annually for maintaining the loan or credit account.

- Overdraft Fees: (Applicable to credit cards and lines of credit) Fees charged when you withdraw more money than available.

- Cash Advance Fees: (Applicable to credit cards) Fees charged for withdrawing cash from a credit card.

These fees can quickly escalate the overall cost, often exceeding the interest paid in some cases.

3. Loan Term: The Duration Factor

The length of your loan (the loan term) directly impacts the total cost. Longer loan terms generally result in lower monthly payments, but you'll pay significantly more in interest over the life of the loan. Shorter loan terms mean higher monthly payments, but substantially less interest paid overall.

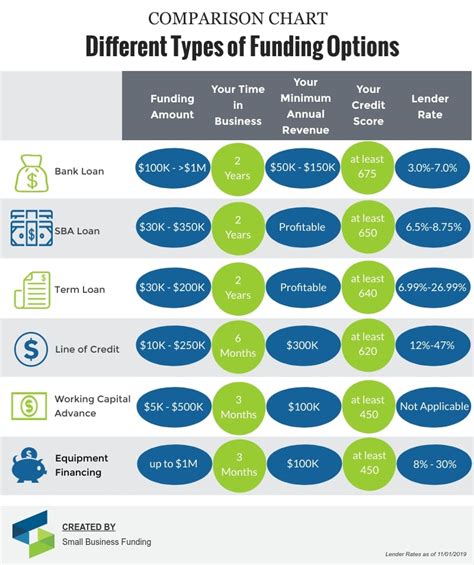

Comparing Financing Options: A Cost Analysis

Let's examine various common financing options and analyze their typical overall costs:

1. Payday Loans: The Most Expensive Option

Payday loans are notoriously known for their exorbitant costs. While convenient for short-term emergencies, they typically charge extremely high interest rates (often exceeding 400% APR) and hefty fees. These fees, combined with the short repayment period, make payday loans the most expensive financing option overall. The high risk of default also leads to potential collection fees and damage to your credit score.

Key Cost Drivers: Extremely high interest rates, substantial fees, short repayment period.

2. Credit Cards: High Interest, Variable Costs

Credit cards offer flexibility but can be expensive if not managed responsibly. Interest rates are typically high, and late payment fees, overdraft fees, and cash advance fees can significantly inflate the total cost. The variable nature of interest rates also makes it difficult to accurately predict the overall cost beforehand. While potentially less expensive than payday loans depending on usage, irresponsible use can quickly lead to overwhelming debt.

Key Cost Drivers: High interest rates (variable), late payment fees, overdraft fees, cash advance fees.

3. Auto Loans: Moderate Costs, Dependent on Credit Score

Auto loans have moderate costs compared to payday loans and credit cards, but the overall expense varies significantly based on your credit score, interest rate, and loan term. A lower credit score leads to higher interest rates and a higher overall cost. Careful comparison of loan terms and interest rates from multiple lenders is crucial to minimize costs.

Key Cost Drivers: Interest rates (influenced by credit score), loan term.

4. Mortgages: Long-Term Commitment, Significant Costs

Mortgages are long-term loans with substantial costs. While interest rates are generally lower than credit cards and auto loans, the sheer length of the loan term (often 15-30 years) means significant interest payments accumulate over time. Closing costs, property taxes, and home insurance further contribute to the overall expense. Despite these high total costs, the long amortization period often makes monthly payments manageable for many.

Key Cost Drivers: Long loan term, high principal amount, closing costs, property taxes, home insurance.

5. Personal Loans: Variable Costs Based on Lender and Credit

Personal loans offer a more flexible approach than secured loans. Interest rates vary greatly depending on your creditworthiness and the lender. Similar to auto loans, a lower credit score results in higher interest rates and fees, directly affecting the overall cost. Shopping around for lenders and comparing terms is essential to minimize expenses.

Key Cost Drivers: Interest rates (influenced by credit score), fees (origination, prepayment penalties, etc.), loan term.

6. Student Loans: Long-Term, Government-Subsidized Options

Student loans can be a significant financial burden, especially with rising tuition costs. While some loans offer government subsidies, others have variable interest rates. Repayment terms span several years, potentially decades, resulting in substantial interest payments over time. Careful consideration of repayment options and budget planning is essential. Forbearance and deferment options can temporarily reduce payments but ultimately extend the repayment period and increase overall interest costs.

Key Cost Drivers: Long loan term, interest rates (variable or fixed), repayment plan choices.

Minimizing Financing Costs: Practical Strategies

Regardless of the financing option you choose, several strategies can help minimize the overall cost:

- Improve your credit score: A higher credit score unlocks lower interest rates and potentially better loan terms across all financing options.

- Shop around for the best rates: Compare offers from multiple lenders before committing to a loan. This is especially critical for auto loans, personal loans, and mortgages.

- Choose a shorter loan term: Although monthly payments will be higher, a shorter loan term significantly reduces the total interest paid.

- Negotiate fees: Don't hesitate to negotiate fees with lenders. Some lenders may be willing to waive or reduce certain fees.

- Pay down debt aggressively: The faster you repay your debt, the less interest you'll pay in the long run.

- Budget carefully: Create a realistic budget to ensure you can afford your monthly payments without incurring late fees or defaulting on your loan.

- Understand the terms and conditions: Read the fine print carefully before signing any loan agreement. Be aware of all fees, interest rates, and repayment terms.

Conclusion: Context Matters

While payday loans consistently demonstrate the highest overall costs due to their predatory interest rates and fees, the "most expensive" financing option ultimately depends on individual circumstances and responsible borrowing practices. Understanding the specific cost components – interest rates, fees, and loan term – is crucial for making informed decisions. By comparing offers from different lenders, improving your creditworthiness, and adopting responsible borrowing habits, you can significantly reduce the overall cost of borrowing and avoid falling into a cycle of debt. Remember that responsible financial planning is key to navigating the complexities of financing and achieving your financial goals.

Latest Posts

Latest Posts

-

When Towing A Trailer On A 65 Mph Posted Highway

Mar 22, 2025

-

Examples Are Especially Helpful As Supporting Materials Because They

Mar 22, 2025

-

Which Of The Following Can Surrender A Deferred Annuity Contract

Mar 22, 2025

-

Artworks Made Using Alternative Media And Processes

Mar 22, 2025

-

A Picture Composed Of Straight And Curved Lines

Mar 22, 2025

Related Post

Thank you for visiting our website which covers about Which Financing Option Has The Highest Overall Costs . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.