In A Dynamic Economy Under Ideal Conditions:

Breaking News Today

Mar 17, 2025 · 5 min read

Table of Contents

In a Dynamic Economy Under Ideal Conditions: A Deep Dive

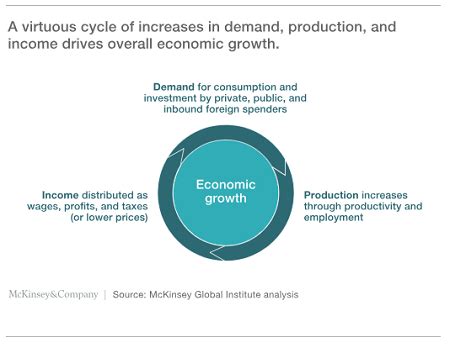

A dynamic economy, characterized by constant innovation, technological advancement, and structural change, thrives under specific ideal conditions. While perfectly ideal conditions rarely exist in the real world, understanding these theoretical benchmarks allows us to analyze and strive for optimal economic performance. This article will explore these ideal conditions, examining their impact on various economic aspects, and discussing the challenges in achieving them.

The Pillars of an Ideal Dynamic Economy

Several key pillars support a thriving dynamic economy under ideal conditions. These include:

1. Perfect Competition: The Engine of Efficiency

Perfect competition, a theoretical market structure, assumes numerous buyers and sellers, homogeneous products, free entry and exit, and perfect information. This environment fosters efficiency because:

- Price Discovery: Prices accurately reflect the balance of supply and demand, preventing artificial inflation or deflation.

- Innovation: Firms constantly strive for efficiency gains to maintain competitiveness, driving innovation and technological progress.

- Resource Allocation: Resources are allocated to their most productive uses, maximizing overall economic output.

- Consumer Sovereignty: Consumers have significant influence on production decisions, ensuring goods and services meet their needs and preferences.

Challenges to Perfect Competition: In reality, monopolies, oligopolies, and other market imperfections hinder perfect competition. Government regulation, intellectual property rights, and economies of scale often create barriers to entry, limiting the number of competitors and potentially leading to higher prices and less innovation.

2. Technological Advancement: The Catalyst for Growth

Technological progress is the lifeblood of a dynamic economy. Under ideal conditions, this progress is:

- Rapid and Consistent: Continuous breakthroughs in various fields fuel productivity growth and create new industries and job opportunities.

- Widely Diffused: New technologies are readily accessible to businesses and consumers, facilitating widespread adoption and maximizing their impact.

- Sustainable: Technological advancements are environmentally responsible and contribute to long-term sustainability, preventing resource depletion and environmental damage.

Challenges to Technological Advancement: The pace and diffusion of technological progress are often uneven. Funding limitations, regulatory hurdles, and a lack of skilled labor can hinder innovation. Moreover, the environmental impact of some technologies raises concerns about sustainability.

3. Flexible Labor Markets: Adapting to Change

A dynamic economy requires a labor market that can adapt quickly to shifting economic conditions. This necessitates:

- Labor Mobility: Workers can easily transition between jobs, industries, and regions, responding efficiently to changing demand.

- Skills Development: Workers possess the necessary skills to meet the evolving demands of the economy, facilitated by accessible and effective education and training programs.

- Wage Flexibility: Wages adjust quickly to reflect changes in productivity and labor market conditions, promoting efficient allocation of labor.

Challenges to Labor Market Flexibility: Rigid labor laws, high unemployment benefits, and skills mismatches can hinder labor mobility and flexibility. Resistance to wage adjustments, particularly downward adjustments, can lead to unemployment and inefficiencies.

4. Stable Macroeconomic Environment: Providing Certainty

A stable macroeconomic environment provides businesses and consumers with the confidence to invest and spend, fostering sustainable growth. Key aspects include:

- Low Inflation: Stable prices prevent uncertainty and encourage long-term planning.

- Low Unemployment: A healthy labor market boosts consumer spending and business investment.

- Stable Exchange Rates: Predictable exchange rates facilitate international trade and investment.

- Sound Fiscal and Monetary Policies: Government policies promote sustainable growth while managing inflation and unemployment effectively.

Challenges to Macroeconomic Stability: External shocks, such as global recessions or commodity price fluctuations, can disrupt macroeconomic stability. Poorly designed government policies, fiscal mismanagement, and financial instability can also lead to instability.

5. Effective Institutions and Governance: Ensuring Fair Play

Strong and efficient institutions are crucial for fostering a dynamic economy. This includes:

- Rule of Law: A fair and predictable legal system protects property rights, enforces contracts, and minimizes corruption.

- Efficient Government: Government intervention is minimal but targeted, focusing on promoting competition, protecting consumers, and addressing market failures.

- Transparency and Accountability: Open and transparent government operations build trust and confidence in the economy.

- Strong Property Rights: Secure property rights encourage investment and innovation.

Challenges to Effective Institutions: Corruption, weak rule of law, and inefficient bureaucracy can stifle economic activity. Lack of transparency and accountability can erode trust and deter investment.

The Interplay of Ideal Conditions

These ideal conditions are not independent; they interact and reinforce one another. For example, perfect competition encourages innovation, which drives technological advancement. Technological advancement, in turn, creates new job opportunities, increasing labor mobility and requiring skills development. A stable macroeconomic environment provides the necessary confidence for businesses to invest in new technologies and expand their operations. Strong institutions ensure fair competition and protect intellectual property rights, further fueling innovation and growth.

Consequences of Departures from Ideal Conditions

When a dynamic economy deviates significantly from these ideal conditions, several negative consequences may arise:

- Reduced Economic Growth: Market imperfections, technological stagnation, and labor market rigidities can significantly hamper economic growth.

- Increased Inequality: Uneven distribution of income and wealth can exacerbate social tensions and political instability.

- Environmental Degradation: Unsustainable technological advancements and a lack of environmental regulation can lead to significant environmental damage.

- Financial Instability: Macroeconomic instability can trigger financial crises and economic recessions.

- Social Unrest: High unemployment, income inequality, and a lack of opportunity can lead to social unrest and political instability.

Striving for an Approaching Ideal

While achieving perfectly ideal conditions is impossible, striving for them remains a crucial goal for policymakers and businesses alike. This involves:

- Promoting Competition: Implementing policies that encourage competition and prevent monopolies, such as antitrust laws and deregulation.

- Investing in Education and Training: Developing a skilled workforce capable of adapting to technological change.

- Enhancing Labor Market Flexibility: Designing labor market policies that promote mobility and reduce unemployment.

- Maintaining Macroeconomic Stability: Implementing sound fiscal and monetary policies to control inflation and unemployment.

- Strengthening Institutions and Governance: Improving the rule of law, reducing corruption, and promoting transparency and accountability.

Conclusion

A dynamic economy under ideal conditions is characterized by rapid technological advancement, efficient resource allocation, and continuous adaptation. While achieving these ideal conditions perfectly is unrealistic, understanding them provides a framework for analyzing economic performance and designing policies that promote sustainable growth, inclusivity, and stability. By continually striving towards these ideals, nations can create more prosperous and equitable societies for their citizens. The journey towards this idealized economic state requires a constant reassessment of policy and a commitment to ongoing adaptation in response to emerging challenges. Ultimately, the pursuit of these ideals is a continuous process of refinement and improvement, driving towards a more robust and resilient global economy.

Latest Posts

Latest Posts

-

The Direct Carry Is Used To Transfer A Patient

Mar 18, 2025

-

The Emancipation Proclamation Of January 1 1863 Quizlet

Mar 18, 2025

-

These Cards Will Get You Drunk Quizlet

Mar 18, 2025

-

Did Quizlet Get Rid Of Q Chat

Mar 18, 2025

-

Myasthenia Gravis Is An Autoimmune Disease In Which Quizlet

Mar 18, 2025

Related Post

Thank you for visiting our website which covers about In A Dynamic Economy Under Ideal Conditions: . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.