The Entry To Close The Expense Accounts Includes

Breaking News Today

Apr 03, 2025 · 5 min read

Table of Contents

The Entry to Close Expense Accounts: A Comprehensive Guide

Closing the books at the end of an accounting period is a crucial step in maintaining accurate financial records. A key part of this process involves closing the temporary accounts, including expense accounts. Understanding the entry to close expense accounts is essential for accurate financial reporting and preparing for the next accounting period. This comprehensive guide will delve into the intricacies of this process, providing a clear and detailed explanation for both beginners and experienced accountants.

Understanding the Nature of Expense Accounts

Before diving into the closing entry, let's solidify our understanding of expense accounts. Expense accounts are temporary accounts that track the costs incurred by a business during a specific accounting period. Unlike permanent accounts (like assets, liabilities, and equity), expense accounts are closed at the end of each period to reset them to zero for the next period. This ensures that the expense amounts for each period are accurately reported on the income statement. Common examples of expense accounts include:

- Rent Expense: Costs associated with leasing a business property.

- Salaries Expense: Payments to employees.

- Utilities Expense: Costs of electricity, water, gas, etc.

- Supplies Expense: Costs of materials consumed during operations.

- Depreciation Expense: Allocation of the cost of assets over their useful life.

- Insurance Expense: Premiums paid for insurance coverage.

- Advertising Expense: Costs associated with marketing and advertising campaigns.

- Travel Expense: Costs incurred on business-related travel.

The Purpose of Closing Expense Accounts

Closing expense accounts serves several vital purposes:

- Accurate Financial Reporting: By closing expense accounts, we ensure that the income statement reflects only the expenses incurred during the specific accounting period. This provides a clear picture of profitability for that period.

- Preparation for the Next Period: Resetting expense accounts to zero at the end of each period prepares them for recording expenses in the upcoming period. This prevents the accumulation of expenses from different periods and ensures accurate tracking of current costs.

- Maintaining the Accounting Equation: Closing entries are vital for maintaining the fundamental accounting equation: Assets = Liabilities + Equity. Closing expense accounts helps balance this equation at the end of each period.

The Closing Entry: A Step-by-Step Explanation

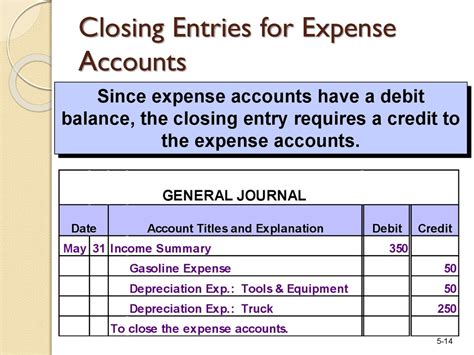

The closing entry for expense accounts involves debiting the Income Summary account and crediting each individual expense account. The Income Summary account is a temporary account used to consolidate all revenue and expense accounts before they are closed. Here's a breakdown of the process:

1. Identify all Expense Accounts: Begin by identifying all expense accounts with a debit balance from the trial balance.

2. Calculate the Total Expenses: Sum the balances of all expense accounts. This total represents the total expenses incurred during the accounting period.

3. Make the Closing Entry: The closing entry will be:

Debit: Income Summary (for the total expenses) Credit: Each Individual Expense Account (for the balance of each account)

Example:

Let's say your trial balance shows the following expense account balances:

- Rent Expense: $5,000

- Salaries Expense: $20,000

- Utilities Expense: $2,000

- Supplies Expense: $1,000

The total expenses are $28,000 ($5,000 + $20,000 + $2,000 + $1,000). The closing entry would be:

Debit: Income Summary $28,000 Credit: Rent Expense $5,000 Credit: Salaries Expense $20,000 Credit: Utilities Expense $2,000 Credit: Supplies Expense $1,000

Understanding the Debit and Credit Impacts

The debit to the Income Summary account increases its debit balance, reflecting the total expenses incurred. The credits to the individual expense accounts reduce their balances to zero, effectively closing them. This is consistent with the normal balance of expense accounts (debit) and the rule that credits decrease debit balances.

The Importance of Accurate Record Keeping

Maintaining meticulous records is crucial throughout the accounting cycle, particularly when closing the books. Inaccuracies in expense account balances can lead to errors in the income statement and ultimately affect the overall financial position of the business. Using accounting software can significantly reduce the risk of errors and streamline the closing process.

Common Errors and How to Avoid Them

Several common mistakes occur when closing expense accounts. These include:

- Forgetting to Close All Expense Accounts: Ensure all expense accounts are included in the closing entry.

- Incorrect Calculation of Total Expenses: Double-check the total expense amount to avoid errors.

- Incorrect Debit and Credit Entries: Carefully review the debit and credit entries to ensure they are correctly recorded.

- Failing to Update the General Ledger: After the closing entry, update the general ledger to reflect the zero balances in the expense accounts.

Regularly reconciling your accounts and performing a trial balance before closing the books can help detect and correct errors early on.

Closing Entries and the Income Statement

The closing of expense accounts is directly linked to the preparation of the income statement. The total expenses, as reflected in the debit balance of the Income Summary account, are used to calculate the net income or net loss for the period. The Income Summary account's balance is then transferred to the retained earnings account (for corporations) or owner's equity account (for sole proprietorships or partnerships) through another closing entry.

Advanced Considerations: Multiple Accounting Periods & Adjustments

In some cases, companies might have multiple accounting periods within a fiscal year (e.g., monthly or quarterly). The closing entry process remains consistent, though it will be repeated for each period. Additionally, adjusting entries might be necessary before closing the books to account for accruals, deferrals, and other adjustments. These adjustments ensure the accuracy of the financial statements.

The Role of Accounting Software

Modern accounting software simplifies the closing process significantly. Many accounting programs automate the closing entries, reducing the manual work and minimizing the risk of errors. Software also provides features for tracking expenses, generating reports, and ensuring the accuracy of financial records. Proper use of this software can significantly improve efficiency and accuracy.

Conclusion: Mastering the Art of Closing Expense Accounts

Closing expense accounts is a fundamental aspect of accounting. Understanding the entry, the reasoning behind it, and the potential pitfalls is vital for accurate financial reporting and effective business management. By following the steps outlined in this guide and maintaining meticulous records, you can ensure the smooth and accurate closing of your expense accounts at the end of each accounting period, leading to more informed financial decision-making. Remember that accuracy is paramount, and taking the time to properly close your books is an investment in the long-term health and success of your business. Regularly review and refine your closing procedures to optimize efficiency and minimize the risk of errors.

Latest Posts

Latest Posts

-

A Patient Has A Blood Pressure Of 130 70

Apr 03, 2025

-

How Are Mortgage And Auto Loans Similar

Apr 03, 2025

-

America The Story Of Us Episode 2 Revolution Answer Key

Apr 03, 2025

-

Phage Typing Is Based On The Fact That

Apr 03, 2025

-

In A Hypersensitivity Reaction What Produces Edema

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about The Entry To Close The Expense Accounts Includes . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.