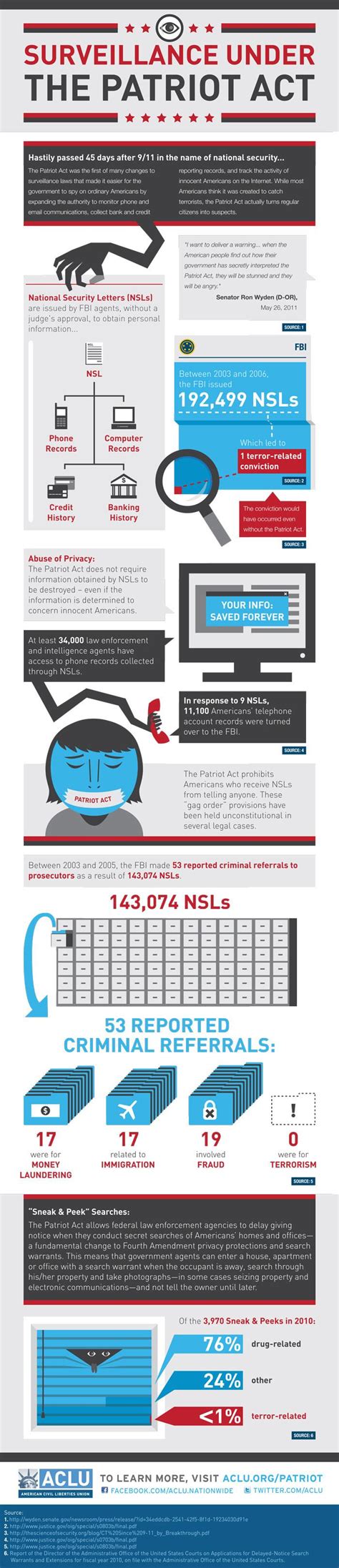

Under The Usa Patriot Act Insurers Are Required To Report

Breaking News Today

Mar 27, 2025 · 6 min read

Table of Contents

Under the USA PATRIOT Act: Insurers and the Duty to Report

The USA PATRIOT Act, officially known as the Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act of 2001, significantly altered the landscape of financial regulation and data sharing in the United States. While primarily focused on combating terrorism and enhancing national security, the Act's provisions have far-reaching implications for various sectors, including the insurance industry. A crucial aspect of the PATRIOT Act's impact on insurers is the requirement to report suspicious activity. This article delves into the specifics of this mandate, exploring its complexities, implications, and ongoing debates surrounding its implementation.

Understanding the Suspicious Activity Reporting (SAR) Requirement

The PATRIOT Act introduced Section 352, which empowers the Secretary of the Treasury to issue regulations requiring financial institutions, including insurance companies, to report suspicious activity. This is not limited to outright acts of terrorism financing; it encompasses a broader spectrum of potentially illicit activities. The primary aim is to detect and deter money laundering, terrorist financing, and other financial crimes.

Key aspects of the SAR requirement for insurers include:

-

Definition of "Suspicious Activity": The regulations provide a broad definition of suspicious activity, encompassing transactions that might involve money laundering, terrorist financing, or other criminal activities. This includes unusual patterns of activity, large cash transactions, structuring of transactions to avoid reporting thresholds, and transactions involving known or suspected terrorists or criminals. The key is whether the activity deviates significantly from the typical behavior of the insured or the nature of the insurance policy itself.

-

Reporting Thresholds: While there aren't specific monetary thresholds that trigger a SAR filing, the focus is on the suspicious nature of the activity, regardless of its size. A small transaction can be just as suspicious as a large one, especially if it aligns with other red flags.

-

Information Required in a SAR: A SAR must include detailed information about the suspicious activity, including the identity of the involved parties, the nature of the transaction, and the reasons why the activity is considered suspicious. The level of detail required is significant, necessitating thorough record-keeping practices by insurers.

-

Confidentiality: Insurers are generally protected from liability for filing a SAR in good faith, even if the reported activity ultimately proves to be innocent. However, this protection doesn't extend to reporting done with reckless disregard for the truth or with malicious intent. The confidentiality aspect is crucial to encourage reporting without fear of retribution.

Types of Insurance Policies Subject to SAR Requirements

The reach of the SAR requirements under the PATRIOT Act isn't limited to a specific type of insurance policy. While the focus might be heightened for policies with larger sums insured or those involving international transactions, virtually all insurance products and services could potentially trigger a SAR filing. Examples include:

-

Life Insurance: Large life insurance policies, especially those purchased with unusual payment methods or beneficiaries who are associated with known high-risk individuals or entities, can draw scrutiny.

-

Health Insurance: While less common, unusual patterns in healthcare claims or payments could potentially warrant a SAR, particularly if they suggest fraud or money laundering.

-

Property and Casualty Insurance: High-value insurance claims involving suspicious circumstances, such as unusually large payouts or claims related to known criminal activities, might necessitate a SAR.

-

Annuities: Similarly to life insurance, annuities with atypical features or beneficiaries could lead to SAR filings.

-

Commercial Insurance: Commercial policies, particularly those involving international business or high-risk industries, are more likely to be subject to enhanced scrutiny and may trigger SAR requirements.

The Role of Insurance Professionals in SAR Compliance

Insurance professionals – from underwriters and claims adjusters to compliance officers – play a pivotal role in ensuring compliance with the SAR requirements. Their diligence and training are paramount in identifying suspicious activity and ensuring prompt and accurate reporting. Training programs should focus on:

-

Identifying Red Flags: Training should cover a comprehensive range of red flags indicating potential money laundering, terrorist financing, or other financial crimes.

-

Understanding SAR Requirements: Insurers must thoroughly understand the specific legal requirements for filing SARs, including the information required and the reporting procedures.

-

Record-Keeping Practices: Maintaining accurate and detailed records is crucial for facilitating effective SAR filings and potential subsequent investigations.

-

Internal Controls: Robust internal controls and procedures are necessary to ensure consistent adherence to SAR requirements and to detect and prevent suspicious activity.

Challenges and Debates Surrounding SAR Reporting by Insurers

Despite the clear intent and purpose of the PATRIOT Act's SAR provisions, several challenges and ongoing debates surround its implementation within the insurance industry:

-

The Subjectivity of "Suspicious Activity": The broad definition of "suspicious activity" can lead to subjective interpretations, potentially resulting in unnecessary or inconsistent reporting. Clearer guidelines and more specific examples of suspicious activities are often desired.

-

Burden on Insurers: The administrative burden associated with implementing and complying with SAR requirements can be substantial, particularly for smaller insurers with limited resources. This includes the costs of training, record-keeping, and reporting.

-

Balancing Security and Privacy: The need to balance national security concerns with the protection of customer privacy and confidentiality is a complex issue that requires careful consideration.

-

Data Sharing and Collaboration: Effective SAR reporting necessitates efficient data sharing and collaboration between insurers, law enforcement agencies, and other relevant stakeholders. Streamlining these processes is crucial for effective enforcement.

-

Technological Advancements: The increasing use of technology in the insurance industry presents both opportunities and challenges. Advanced analytics can be used to identify suspicious patterns, but this requires investments in technology and expertise.

The Future of SAR Reporting in the Insurance Sector

The landscape of SAR reporting for insurers is constantly evolving. Ongoing efforts to refine regulatory guidelines, enhance training programs, and improve data-sharing mechanisms are critical for improving the effectiveness of the system. This also includes focusing on the use of AI and machine learning to identify and flag potentially suspicious activities, enhancing the efficiency and accuracy of SAR reporting. The emphasis will likely continue to be on a risk-based approach, prioritizing investigations into the most concerning activities while managing the burden on insurers efficiently. Furthermore, increased international cooperation will likely play a crucial role in combating transnational financial crimes.

Conclusion

The USA PATRIOT Act's requirement for insurers to report suspicious activity plays a critical role in combating financial crime and protecting national security. While the complexities and challenges of implementing these requirements are significant, the ultimate aim is to foster a safer and more secure financial system. Through diligent training, robust internal controls, and ongoing improvements in regulatory guidance and technology, insurers can effectively manage their compliance obligations while maintaining the integrity and trust of their clients. The ongoing dialogue and evolution of the SAR framework ensure its adaptability to the changing dynamics of financial crime in the digital era, continuously balancing national security imperatives with the rights and expectations of individuals and businesses.

Latest Posts

Latest Posts

-

Correctly Label The Following Parts Of The Digestive System

Mar 30, 2025

-

Locking Out Tagging Out Refers To The Practice Of

Mar 30, 2025

-

How Has Globalization Made Countries More Interdependent Choose Five Answers

Mar 30, 2025

-

The Term Meaning Above Or Outside The Ribs Is

Mar 30, 2025

-

File Compression Is Useful For Select All That Apply

Mar 30, 2025

Related Post

Thank you for visiting our website which covers about Under The Usa Patriot Act Insurers Are Required To Report . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.