Which Of The Following Factors Determine Depreciation

Breaking News Today

Apr 03, 2025 · 6 min read

Table of Contents

Which Factors Determine Depreciation? A Comprehensive Guide

Depreciation, the systematic allocation of an asset's cost over its useful life, is a crucial accounting concept impacting financial statements and tax obligations. Understanding the factors that influence depreciation is essential for accurate financial reporting and informed business decisions. This comprehensive guide delves into the multifaceted nature of depreciation, exploring the key determinants that shape its calculation.

The Core Factors Influencing Depreciation

Several key factors interact to determine the depreciation expense recognized each period. These can be broadly categorized as:

-

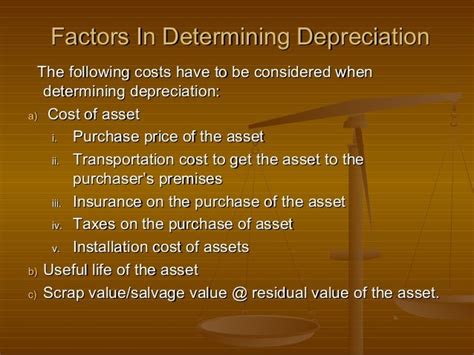

Cost of the Asset: This is the initial outlay incurred to acquire and prepare the asset for its intended use. It includes the purchase price, transportation costs, installation fees, and any other expenses directly attributable to getting the asset ready for operation. Higher cost inherently leads to higher depreciation expense.

-

Useful Life: This represents the estimated period over which the asset is expected to provide economic benefits to the business. Estimating useful life requires careful consideration of factors like technological obsolescence, physical wear and tear, and legal or regulatory limitations. A shorter useful life translates to higher annual depreciation. The selection of useful life is a critical judgment call and can significantly impact the financial statements.

-

Salvage Value (Residual Value): This is the estimated value of the asset at the end of its useful life. It's the amount the company expects to recover from the asset's sale or disposal after it's no longer useful. Higher salvage value results in lower depreciation expense. Accurately estimating salvage value is challenging, as it depends on unpredictable future market conditions.

-

Depreciation Method: Several methods exist for calculating depreciation, each with its own assumptions and implications. The choice of method significantly influences the depreciation expense recognized each year. The most common methods include:

-

Straight-Line Depreciation: This is the simplest method, allocating equal depreciation expense over the asset's useful life. It's calculated as:

(Cost - Salvage Value) / Useful Life. It's straightforward but may not accurately reflect the asset's actual decline in value. -

Declining Balance Depreciation: This is an accelerated depreciation method, resulting in higher depreciation expense in the early years of the asset's life and lower expense in later years. It uses a fixed depreciation rate applied to the asset's net book value (cost less accumulated depreciation) each year. This method reflects the faster rate of obsolescence experienced by many assets. A common variant is the double-declining balance method, which uses double the straight-line rate.

-

Units of Production Depreciation: This method bases depreciation on the asset's actual usage or output. The depreciation expense is calculated per unit produced, multiplying this rate by the number of units produced during the period. This is suitable for assets whose value is directly related to their output, such as machinery.

-

Sum-of-the-Years' Digits Depreciation: Another accelerated method, this allocates higher depreciation in the early years. The formula involves summing the digits of the asset's useful life and using a fraction based on this sum.

-

The choice of method depends on the specific circumstances and the nature of the asset. Management's judgment plays a significant role in selecting the most appropriate method that best reflects the asset's pattern of consumption.

Beyond the Core Factors: Other Influences on Depreciation

While the core factors above form the foundation of depreciation calculations, several other elements subtly or significantly influence the process:

-

Technological Obsolescence: Rapid technological advancements can render assets obsolete before the end of their physical useful life. This necessitates shorter useful lives and increased depreciation expense to reflect the reduced economic value. Industries experiencing rapid technological change, like electronics or software, often face higher depreciation rates due to obsolescence.

-

Physical Wear and Tear: The physical condition of an asset influences its useful life. Assets subjected to heavy use or harsh operating conditions will likely deteriorate faster, leading to shorter useful lives and higher depreciation. Regular maintenance and repairs can mitigate wear and tear but won't eliminate it entirely.

-

Economic Conditions: Broad economic factors like inflation and interest rates indirectly affect depreciation. Inflation can influence the replacement cost of assets, potentially impacting the perceived useful life and salvage value. Interest rates also play a role in capital budgeting decisions, affecting the investment timeline and asset replacement strategies.

-

Company Policy: A company's internal accounting policies can influence the choice of depreciation methods and the estimation of useful lives and salvage values. Consistent application of these policies is critical for ensuring the comparability of financial statements over time.

-

Industry Practices: Industry-specific norms and regulations can impact depreciation practices. Certain industries might adopt particular methods or guidelines for depreciation, influencing the consistency and comparability of financial statements across competitors.

-

Tax Regulations: Tax laws and regulations often dictate allowable depreciation methods and rates for tax purposes. These regulations can differ from generally accepted accounting principles (GAAP), leading to differences between book depreciation and tax depreciation.

The Impact of Depreciation on Financial Statements and Decision-Making

Depreciation significantly affects a company's financial statements and plays a crucial role in various business decisions:

-

Income Statement: Depreciation is an expense that reduces net income. The choice of depreciation method directly impacts reported earnings, affecting profitability metrics and investor perception. Accelerated depreciation methods lead to lower net income in early years, while straight-line depreciation spreads the expense evenly.

-

Balance Sheet: Accumulated depreciation, the total depreciation expense recognized over an asset's life, is reported as a contra-asset account, reducing the asset's book value. This affects the company's total assets and equity.

-

Cash Flow Statement: Depreciation is a non-cash expense, meaning it doesn't directly impact cash flow. However, it indirectly influences cash flow by affecting net income, which is a component of the cash flow from operations.

-

Capital Budgeting Decisions: Depreciation impacts capital budgeting decisions by influencing the calculation of net present value (NPV) and internal rate of return (IRR) of investment projects. Accurate depreciation estimates are critical for making informed capital investment decisions.

-

Tax Implications: Depreciation is a tax-deductible expense, reducing taxable income and ultimately tax liability. Different depreciation methods can have significant tax implications, leading to variations in the timing of tax savings. Companies strategically choose depreciation methods to optimize tax benefits within legal and regulatory constraints.

Addressing Challenges in Depreciation Estimation

Estimating depreciation involves inherent uncertainty. Accurately predicting an asset's useful life and salvage value can be challenging, particularly in dynamic economic environments and rapidly changing technological landscapes. To mitigate this, businesses employ several strategies:

-

Regular Review and Adjustment: Depreciation estimates should be periodically reviewed and adjusted based on actual asset performance, technological advancements, and economic conditions. This ensures that depreciation reflects the asset's current economic value.

-

Sensitivity Analysis: Performing sensitivity analysis by varying assumptions about useful life and salvage value helps assess the impact of these estimates on depreciation and financial statements. This provides a range of possible outcomes, improving decision-making under uncertainty.

-

Expert Consultation: Consulting with industry experts or specialized valuation professionals can provide valuable insights into estimating useful life and salvage value, enhancing the accuracy of depreciation calculations.

Conclusion: Depreciation – A Multifaceted Process Requiring Careful Consideration

Depreciation is a complex process influenced by various intertwined factors. Understanding these factors is crucial for accurate financial reporting and informed business decisions. The choice of depreciation method, estimation of useful life and salvage value, and consideration of external factors significantly impact the financial statements and tax obligations. By carefully considering these factors and employing robust estimation techniques, businesses can ensure their depreciation calculations accurately reflect the economic reality of their assets. Regular review, sensitivity analysis, and expert consultation can further enhance the accuracy and reliability of depreciation estimates, ultimately contributing to sound financial management and strategic planning.

Latest Posts

Latest Posts

-

Pal Cadaver Appendicular Skeleton Upper Limb Lab Practical Question 3

Apr 04, 2025

-

If A Test Is Standardized This Means That

Apr 04, 2025

-

A Week After A Full Moon The Moons Phase Is

Apr 04, 2025

-

Ap Chemistry Unit 7 Progress Check Mcq

Apr 04, 2025

-

Which Of The Following Road Surfaces Freezes First

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about Which Of The Following Factors Determine Depreciation . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.