A Mortgage Loan Originator Is Not Prohibited From

Breaking News Today

Apr 02, 2025 · 6 min read

Table of Contents

A Mortgage Loan Originator is Not Prohibited From… A Comprehensive Guide

A mortgage loan originator (MLO) plays a crucial role in the home buying process, guiding clients through the complexities of securing a mortgage. While heavily regulated, there are many activities MLOs are permitted to do, often misunderstood as prohibited. This comprehensive guide clarifies these areas, offering a nuanced understanding of an MLO's permissible actions and responsibilities. Understanding these boundaries is vital for both MLOs seeking to maintain compliance and consumers seeking to navigate the mortgage process effectively.

Understanding the Regulatory Landscape

The mortgage industry is heavily regulated, primarily by the Consumer Financial Protection Bureau (CFPB) and various state licensing agencies. These regulations exist to protect consumers from predatory lending practices and ensure transparency throughout the mortgage process. The key legislation impacting MLOs is the Real Estate Settlement Procedures Act (RESPA) and the Truth in Lending Act (TILA), both designed to promote fair and honest lending.

Key Regulatory Bodies:

- Consumer Financial Protection Bureau (CFPB): The primary federal regulator overseeing the mortgage industry, setting national standards and enforcing compliance.

- State Licensing Agencies: Each state has its own licensing and regulatory requirements for MLOs, adding another layer of compliance.

What a Mortgage Loan Originator IS Allowed To Do

MLOs have a broad range of permissible activities, but it's crucial they operate within the confines of the law and ethical practices. Let's explore several key areas:

1. Providing Comprehensive Financial Advice (within ethical and legal boundaries)

While MLOs aren't financial advisors per se, they can and should provide clients with relevant financial guidance related to their mortgage options. This includes:

- Explaining different mortgage types: Clearly outlining the pros and cons of various loan programs, such as fixed-rate, adjustable-rate, FHA, VA, and conventional loans. This is crucial for informed decision-making.

- Analyzing borrowers' financial situations: MLOs can help borrowers assess their debt-to-income ratio (DTI), credit score, and overall financial health to determine their loan eligibility and affordability. This requires careful data handling and adherence to privacy regulations.

- Discussing long-term financial implications: MLOs should discuss the long-term costs of a mortgage, including principal, interest, taxes, and insurance (PITI), and the potential impact on the borrower's overall financial picture. Transparency is paramount.

2. Negotiating with Lenders on Behalf of Clients

While the final loan terms are determined by the lender, MLOs can advocate for their clients' best interests during the negotiation process. This may involve:

- Exploring various loan options and rates: MLOs can shop around for the best rates and terms from different lenders to ensure their clients secure the most favorable mortgage possible.

- Negotiating closing costs: While MLOs cannot control all closing costs, they can work with lenders to minimize expenses whenever possible, and explain the associated costs transparently.

- Addressing loan contingencies: MLOs can help navigate potential challenges or obstacles that may arise during the loan process. This could involve working with the lender to address credit issues or appraisal discrepancies.

3. Providing Accurate and Timely Information

MLOs have a legal and ethical obligation to provide clients with accurate and timely information throughout the entire mortgage process. This includes:

- Explaining all loan documents clearly and concisely: MLOs should ensure borrowers understand the terms and conditions of their mortgage, avoiding complex jargon or misleading information.

- Responding promptly to client inquiries: Timely communication is crucial for building trust and maintaining a positive client relationship.

- Keeping clients informed of the loan's progress: Regular updates on the application's status can reduce anxiety and uncertainty.

4. Maintaining Confidentiality

MLOs are bound by strict confidentiality rules regarding their clients' financial information. This means that sensitive data must be protected and used solely for the purpose of processing the mortgage application. This includes compliance with:

- Fair Credit Reporting Act (FCRA): MLOs must adhere to FCRA guidelines regarding the handling and use of credit reports.

- Privacy regulations: This includes following relevant federal and state regulations related to data security and privacy.

5. Referring Clients to Other Professionals (With Proper Disclosure)

MLOs may refer clients to other professionals, such as real estate agents, insurance brokers, or attorneys. However, it is crucial to disclose any referral fees or compensation received for these referrals. This ensures full transparency and avoids potential conflicts of interest.

6. Utilizing Technology to Streamline the Process

MLOs are not prohibited from utilizing technology to streamline the mortgage process. This can include:

- Online application portals: Offering convenient and user-friendly online applications.

- Digital document management: Utilizing secure platforms for storing and sharing sensitive client information.

- Automated underwriting systems: Employing technology to expedite the loan approval process.

7. Marketing and Advertising (Within Regulatory Guidelines)

MLOs can market and advertise their services, but they must do so ethically and in compliance with all applicable regulations. This includes:

- Truthful and accurate advertising: Avoiding misleading or deceptive marketing practices.

- Compliance with advertising regulations: Adhering to guidelines from the CFPB and other regulatory bodies.

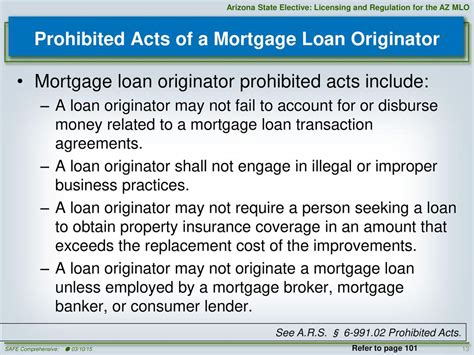

Activities MLOs ARE Prohibited From

To fully understand the permissible actions, it’s equally important to highlight what MLOs are strictly prohibited from doing:

- Steering: Influencing a borrower towards a specific loan product solely for the MLO's benefit (e.g., higher commission).

- Misrepresenting loan terms: Providing inaccurate or misleading information about interest rates, fees, or loan conditions.

- Engaging in predatory lending practices: Exploiting borrowers through unfair or deceptive lending practices.

- Failing to disclose conflicts of interest: Not disclosing any financial relationships that could influence loan decisions.

- Violating consumer privacy laws: Misusing or mishandling sensitive client information.

- Unlicensed or unregistered activities: Operating without the proper state and federal licenses and registrations.

Navigating the Ethical Considerations

Beyond the legal regulations, ethical conduct is paramount for MLOs. Building trust with clients requires:

- Transparency: Openly communicating all aspects of the mortgage process.

- Integrity: Acting honestly and fairly in all dealings.

- Objectivity: Providing unbiased advice and recommendations.

- Competence: Maintaining a high level of professional expertise.

By upholding these ethical standards, MLOs not only comply with regulations but also build long-term relationships based on trust and mutual respect.

Conclusion: A Balanced Approach to Compliance

The role of a mortgage loan originator is complex, demanding a thorough understanding of both legal regulations and ethical practices. While many actions are permissible, the focus should always remain on consumer protection, transparency, and ethical conduct. This guide provides a foundational understanding of what an MLO is not prohibited from doing, emphasizing the crucial balance between permissible activities and maintaining the highest standards of professionalism and integrity. By adhering to both legal and ethical guidelines, MLOs can effectively serve their clients while maintaining compliance within the dynamic mortgage industry. Continuous professional development and staying updated on regulatory changes are essential for success in this field. This continuous learning ensures MLOs can provide the best possible service and avoid potential pitfalls associated with non-compliance.

Latest Posts

Latest Posts

-

Community Health Care Can Provide All Of The Following Except

Apr 03, 2025

-

Which Statement About The Need For Faster Speed To Market Is True

Apr 03, 2025

-

What Hardware Is Essential To Creating A Home Wi Fi Network

Apr 03, 2025

-

Allocating Common Fixed Expenses To Business Segments

Apr 03, 2025

-

What Percentage Of Your Gross Salary Does The Consumer Financial

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about A Mortgage Loan Originator Is Not Prohibited From . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.